1. Introduction

inancial industry including its services and deliveries have witnessed rapid transformation in the recent years due to advancement in technological tools. The reasons are not far-fetched, as there are needs for readily available services that are fast, convenient and more efficient. More also, the combination of the financial services and technology has deepened financial inclusion at ease. Aside alternative digital channels provided by traditional banks to deliver fintech-like services, the common Fintech brands are Stripe (U.S), Coinbase (US), Monzo (UK), Revolut (UK) Flutterwave (Nigeria), Paystack (Nigeria), Lendingkart (India), Instamojo (India),Lufax (China), WeLab (China), Yoco (South Africa) and Zoona (South Africa).. Fintech is the deployment of technology to aid financial transactions such as payments, transfers and lending. They make financial services easier to use, cheaper in most cases, reliable and within consumers reach.

Basically, adoption of Fintech will depend on degree of perceived benefits and perceived risk. Fintech services are readily adopted when the perceived benefits are greater than the perceived risk. Perceived benefits and perceived risks have been classified to different numbers by various researchers under various theories such as Technology Adoption Model (TAM), Elaboration likelihood Model (ELM), Unified Theory of Acceptance and Use of Technology (UTAUT), Theory of Reasoned Action (TRA) and Diffusion of Innovation Theory. Typical fintech adoption research will be carried out utilizing benefits such as ease of use, usefulness of services, financial/economic benefit such as pricing, social influence, speed of transaction (seamless) and convenience. Also, perceived risk is often considered under financial risk (loss of fund), regulatory risk (uncertainty in case of legal issues), security and privacy (how secured and vulnerable is the fintech platform and exposure of personal information) and operational risk (failure in system, processes). Combining the benefits and risks, benefit-risk system (valence level) is drawn to show level of Fintech adoption. Aside perceived risks, others mitigants in Fintech adoption is trust and fintech brand. Fintech adoption research is quantitative in approach while relationship among variables is explore numerically. Investigative hypotheses is developed along the research focus and they will be tested to show significant and non-significant relationships.

Author: e-mail: [email protected] Such investigative research does the following:

1. Confirm the rate at which Fintech services are adopted. 2. Identify differences between variables that influence the behaviour of fintech adoption. 3. Give full consideration to effect of perceived benefits and risks as they set disparity. 4. Bias in adoption of fintech services (payments, microlending, wealth management, insurance, health service, account opening and investments) at the expenses of others. 5. Ascertain constraints faced by financial consumers while they are using Fintech services.

2. II.

3. Literature Review and Theoretical Background

As noted by Alt et al 2018, fintech exist when financial services are combined with delivering technologies. The overall aim is to coordinate activities and processes in a standardize manner such that intended financial tasks are performed efficiently. Many theories have been applied to justify adoption of Fintech among financial consumers such as Theory of reasoned action (TRA), Technology Acceptance Model (TAM), Diffusion Theory and Unified Theory of Acceptance and Use of Technology (UTAUT). Most researchers in the recent years focus more on UTAUT which has more power to absorb complex research questions and objectives. Review will be made of TAM model as one of the theories which were combined to invent UTAUT. Also, TRA, Theory of Planned Behaviour TPB and Theory of Perceived Risk are often integrated to justify constructs used for perceived risks in some research hypotheses. Diffusion Theory is itemized to actually reveal different levels of technology adopters and justify why everybody will not adopt technology at the same time. This can be used to study adoption behaviour and pattern.

4. a) Technology Acceptance Model (TAM)

The theory was developed by Fed Davis in 1989 in his doctoral thesis at MIT. TAM has been judged as the most widely used theory in Information System to back adoption of various innovation and invention in Financial Technology. The popularity and widely acceptance of the theory is due to the fact that the theory was particularly invented to study adoption and implementation of technology that financial transactions relied on. The whole system of the model is unambiguous and simple to use. Dave in his TAM theory, itemized system uses as feedback that is supported by motivation from the users where this motivation further depends on stimulus from the environment.

5. Stimulus

Organization Response Figure 1: Background graphics depicting TAM (Davis, 1985) Motivation from user is divided to three which are 1. Perceived Ease of Use (PEOU) -level at which individual financial users expect the target system is used effortless 2. Perceived Usefulness (PU) -belief by user that making use of the new system will enhance his/her performance and value will be delivered 3. Attitude toward using the system in the various application of the model. As beautiful and widely accepted as TAM theory is, the weakness lie in the fact that social and organization factors were not accommodated in its construct. Perhaps these two factors have considerable impact in influencing innovation in technology and its adoption.

6. b) Theory of Reasoned Action, Theory of Planned Behaviour and Theory of Perceived Risk

Theory of Planned Behaviour is an extension of Theory of Reasoned Action while TRA stated the important role attitude takes in consumers intention to engage in some behaviours (Ajzen 1991), TPB extends the theory by adding perceived behavioural control (Taylor & Todd, 1995). This indicated existence of factors that can aid or hinder performance of a certain behaviour. Some behaviour of an individual performance depends on personal intention which is affected by attitudes and subjective norms (Sanayei & Bahmani, 2012). Conclusively Ajzen and Fishbein 1977, affirmed that an individual with strong believe in positive outcomes will exhibit positive attitude about the behaviour, while negative attitude will be shown when individual expects negative consequences such as loss in perceived risk. Perceived risk is uncertainty that might lead to loss in future. Theory of perceived risk was initially proposed by Bauer in 1960 to describe consumer behaviour considering perceived risk in subject term. Over the years, more studies from Cox (1964,1967) The most suitable philosophy for the proposed research on Fintech adoption is Interpretivim. Aside being commonly used in research philosophy in complex business studies, it is utilized to interpret potential financial user's intentions, perceptions and their actions with respect to Fintech services. As confirmed by Remneyi, 1998, interpretivism is seen as means of monitoring reality behinds selected situation. Most researches in Fintech adoption intend to study adoption pattern without any generalization of the outcomes.

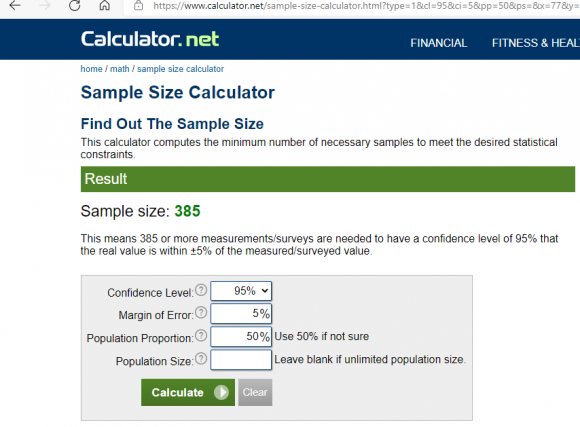

7. a) Sampling Sample Size

There are various ways of determining sample size as justified in past researches. Some are calculative while others follow rule of thumb. The first approach to our sample size as sample to variable ratio. Hair et al, stated the preserved ratio to be 15. Since our of use and its satisfactory outcomes. Making use of calculator.net with the applicable parameters is shown below. With this, the number of respondents for the research work will produce confidence level of 95%. Fintech adoption study is quantitative and Structural Equation Model is often used in treating the linkages among the constructs and the dependent variable, thus sample size below 200 will not be suitable (Kline 2005 and Kline 2016).

8. b) Methods of Data Collection

For proper conduct of fintech adoption research study, empirical data will be collected using questionnaire survey approach. Questionnaire survey is very suitable for acquiring data in Information Science as related by Chen Lin, 2019. Bryman, 2013, a questionnaire survey will allow us collect large amount of data needed for this investigation in order to appropriately mask behaviours of fintech users. Questionnaire can be easily processed statistically and result analyzed with much convenience. The research will make use of convenient sampling technique to carry out the survey. Convenient sampling is efficient, simple to use and implement as questionnaire will only be shared among users that are conveniently available for the study. Convenience sampling is regularly used in the field of social science due to its proximity, accessibility, willingness and quick response (Jager et al, 2017).

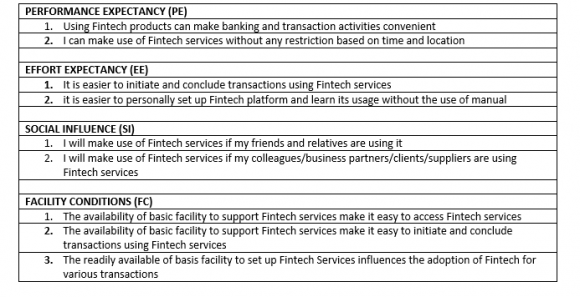

Most fintech adoption research is to analyze important factors which impact adoption of Fintech services. The investigation to analyze behavioural intentions of users will be achieved empirically by collecting data through survey method. Specifically, survey method is chosen, being a quantitative data collection technique used to collect data that are closeended in nature from selected respondents. Many research studies in Fintech adoption subject area used quantitative research methodology as claimed by Noofa et al, 2020 and thus, most researches align with that stand. The survey questionnaire will be prepared by the researchers and administer to financial users on the field. The questions will be interval-based (Likert Scale).

The key segment of the questionnaire will be drafted to investigate the factors influencing the user adoption of Fintech services based on model selected (TAM, UTAUT, TRA, TPB and TPR). Each item bundled under the factor questions is delivered in Likert format. Most study use 7-point Likert scale. This will improve reliability to optimum level (Joshi et al, 2015).

9. c) Sampling Method

The sampling method to be used commonly used in Fintech adoption research is convenience sampling. The investigator (s) prioritized selection of the respondents based on users that are much willing and ready to complete the questionnaire. It is a non-probability method used by researchers to make sample from people that are in a close proximity (Etikan et al, 2016). Also, large sample size is needed to form research deduction based on convenience sampling.

10. d) Sample Research Hypothesis

Research hypothesis are formulated from the constructs of the selected model. Sample below is shown below As stated in UTAUT model to measure robustness of the new technology in when compared to its ease of use. In order to make sure content validity and survey questions are relevant and suitable, pilot test is carried out. This will be reviewed by expert against targeted measures. Also, all proposed constructs is tested using Cronbach alpha coefficient for acceptability.

11. Cronbach Coefficient

Internal Consistency 0.9 and above Excellent 0.8 -0.9 Good 0.7 -0.8 Acceptable 0.6 -0.7 Questionable 0.5 -0. 6 Poor

In many research work, confirmatory factor analysis is used to test model. Also, convergent validity and discriminant validity is carried out. Convergent validity will show correlation extent of multiple indicators for a specific variable. This is done by measuring average variance extracted (AVE). AVE measures of the sample should be greater than 0.5 to indicate convergency in applicable constructs. Discriminant validity indicates no linkage between each variable (measures of each variable can be distinguish from one another). It is tested by evaluating that AVE is greater than the squared interscale correlation for all constructs.

Similarly, composite reliability (CR) and Cronbach's alpha is used to test internal consistency of the data collected. For the proposed model to show good internal consistency CR should be greater than 0.7 and Cronbach's alpha should be greater than 0.8 (Fornell & Larcker, 1981).

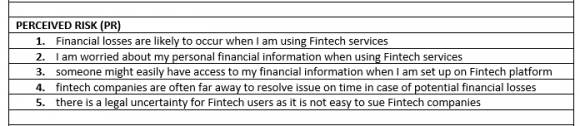

| behaviour. |

| 1. Financial Risk |

| 2. Security Risk |

| 3. Operational Risk |

| 4. Legal Risk |

| The proposed research questionnaire can |

| bedrafted based on these four classes of the perceived |

| risk. |

| Discussion on Fintech Adoption Research | ||||

| Year 2022 | ||||

| Volume XXII Issue I Version I | ||||

| ( ) A | ||||

| Global Journal of Management and Business Research | S/n 1. 2. 3. 4. | Research Title Factors influencing the adoption of Internet Banking Applying Theory of Perceived Risk and Technology Acceptance Model in the online shopping channel Extending the Unified Theory of Acceptance and Use of Technology Understanding Benefit and Risk Adopters Framework of Fintech Adoption: Comparison of Early Adopters and Late | Author (s) S. Naimi Baraghani Huang Jing-Wen and Yong-Hui Li V Venkatesh, J. Thong, Xin Xu Hyun-Sun Ryu | Year 2008 2009 2012 2018 |

| Tun-Pin Chong | ||||

| Keng-Soon William Choo | ||||

| 5. | An adoption of Fintech Services in Malaysia | Yen-Sun Yip Pui-Yee Chan | 2019 | |

| Hong-Leong Julian The | ||||

| Shwu-Shing Ng | ||||

| © 2022 Global Journals | ||||

| Discussion on Fintech Adoption Research | ||||

| Adoption Intention of Fintech Services for | ||||

| 6. | Bank Users: An empirical examination with an extended technology acceptance | Hu Z. D | 2019 | |

| model | ||||

| Factors Influencing attitudes and intention | ||||

| 7. | to adopt financial technology services among the end-users in Lagos State, | Yusuf Opeyemi Akinwale & Adam Konto Kyari | 2020 | |

| Nigeria | ||||

| 8. | Perceived Risk Factors affect intention to use Fintech | Ooi Chee Keony | 2020 | |

| Fintech Revolution, Perceived Risks and | ||||

| 9. | Fintech Adoption: Evidence from Financial | Asima Saleem | 2021 | |

| 10. | Industry of Pakistan Evaluating Drivers of Fintech Adoption in the Netherlands | Rasheedul Hassan Lingli Shao Muhammad Ashfaq | 2021 | Year 2022 |

| Volume XXII Issue I Version I | ||||

| ( ) A | ||||

| Global Journal of Management and Business Research | ||||

| i. | ||||

| © 2022 Global Journals | ||||

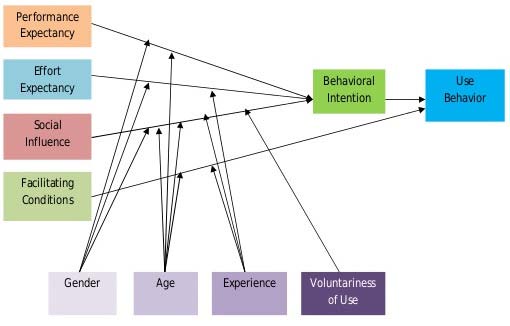

| Hypothesis Number | Hypothesis | Linking Models to Research Questions |

| Performance Expectancy will have significant | Performance Expectancy as mentioned in UTAUT | |

| H1 | influence on use intention of Fintech services | which is analogous Perceived Usefulness in TAM |

| among financial users. | model | |

| H2 | Effort expectancy will have significant influence on use intention of Fintech services among financial users | Effort Expectancy as mentioned in UTAUT which is analogous Perceived Ease of Use in TAM model |

| H3 | Social influence will have significant influence on use intention of Fintech services among users | As stated in UTAUT model to measure influence from family, friend and colleague |

| Facility conditions will have significant influence | ||

| H4 | on effort expectancy of Fintech services among | |

| users |