1. Introduction

he emergence and essence of technology have changed banking services like opening an account, authorizing customer, and transaction processing and recording (Irechukwu, 2000).

With that transformation, the banking sector became digitized with E-Banking, also known as internet banking, online banking, virtual banking, and electronic fund transfer (EFT). Distinct E-Banking products and utilities come forth, namely Automated Teller Machine (ATM), Tele-Banking, Digital Card and Wallet, Electronic Bill Payment, e-cheque, etc. (Daniel, 1999;Mols 1998;Sathye, 1999).

E-Banking is regarded as the cheapest delivery channel mostly, PC, Telephone, Internet, and other electronic media, thereby saving time and cost both for the bank and customer (Markku, 2012 and Al-Smadi and Al-Wabel, 2011). Moreover, E-banking is beneficial to the environment as electronic transmissions un necessitate paper, vehicle traffic, and physical branches. In terms of adoption level, it is evident that because the early embracement of e-banking by the developed countries made it benefited and experienced it (Zhao et al., 2008). It is transparent that the acceptance and exertion of e-banking in most developed countries have matured considerably.

Developing countries like Bangladesh are also quickly adopting and have reached far in Electronic banking service efficiency as experts found it a costefficient system that enables better bank services. Bangladesh experienced a transitional period in the banking sector with digitization, eliminating the drawbacks faced by customers earlier, such as limited accessibility, time consuming customer service, higher cost, etc., (Ali and Akter, 2010).

Despite the progress, e-banking is less or to somehow unknown concept to a noticeable number of customers, choose to go with the traditional way, and not all the branches of banks are fully functional to this system. Researchers tried to understand what made people uncomfortable to put a deal with it. Be sides less awareness, inadequate training on using electronic media and the internet, Poor marketing effort, etc. could be the barrier to the advancement of E-Banking here. This paper aims at surveying customer satisfaction and attitude over e-banking performance in Bangladesh as well as explore the history and current scenario of it in Bangladesh.

The key research question of this paper is to understand the extent of customer satisfaction concerning the adoption of E-banking in Bangladesh. To facilitate the main objective, few supporting objectives have been considered. They are to provide an overview of the existing e-banking infrastructure of Bangladesh, the exhibition of the current scenario, the expansion of e-banking in Bangladesh, and outline recommendations for the concerned. Section two deals with the current status of e-banking practices in Bangladesh, section three is about literature review and research methods used, section four discusses the analysis and findings and section five summarizes conclusion remarks, and relevant recommendations.

2. a) The Status of E-Banking in Bangladesh

The banking industry of Bangladesh, structured with 57 scheduled banks as of December Also, the dynamic website of BB offers open data sources. To mobilize payment and settlement systems, the Payment Systems Department (PSD) of Bangladesh Bank functions with an automated processing system, national payment switch, Real-time gross settlement, mobile financing, e-commerce, mcommerce, payment systems strategy. In most re-cent, BB has launched the Interbank Internet Banking Fund Transfer or IBFT service.

3. Literature Review

The e-banking system has evolved in different ways; branched on the ground of the instruments used. By using a telephone connection, electronic banking, categorized as Phone Banking, Automated Telephone System, Mobile Banking (SMS banking, GSM Toolkit. whereas Home Banking, Internet banking, Online Banking, Mail Banking falls under electronic banking with Personal Computer. (Chovanová, 2006). E-Banking services are carried through versatile electronic means collectively called Electronic delivery channels, which are: Electronic Fund Transfer, Any Branch Banking, Point of Sale (POS), KIOSK, SWIFT, and Magnetic Ink Character Recognition (MICR), open online, Money Link, Phone Link, ATM, Credit Cards, Debit Cards (Bashir et al., 2015).

The banking sector of Bangladesh has adopted several policies and instructions integrated by Bangladesh Bank, the central bank of Bangladesh, in all possible areas under sustainable banking (Bangladesh Bank, 2016). Green banking is one of three broad categories of sustainable banking, and this category has achieved a high status in the era of ebanking services. 100% of banks in Bangladesh have now online branches, and 72.9% of these are fully online (Bangladesh Bank, 2016). Undoubtedly, e-banking has brought a revolutionary flavor to banking customer services. But the success of such a paramount program is not possible until the demand section finds it fit. The customers' satisfaction in e-banking services receives consistent attention from the researchers as technology and service patterns change daily.

A large volume of researches focused to understand the variety of dimensions of e-banking services ( But, researchers do not even respond to customers' satisfaction seams about e-banking services throughout developing countries. Researchers found that electronic banking service channels have gained a positive impression in India and Kenya (Nyangosi et al.,2009) as well as the failure of achieving customers'responses (Rashmita and Saho, 2013). To some extent, insisting on products and services become more important rather than a better customer experience cause of the marketing strategy (Rashmita and Saho, 2013). But, service quality and informational trust are the keys to deliver satisfactory customer services (Islam and Yang, 2009). Bangladesh is a growing economy, with 58 scheduled banks (Bangladesh Bank, 2017). In such a competitive situation, this research aims at revealing the customer's experience of e-banking products and services.

4. III.

5. Research Method a) Research Technique

Both quantitative and qualitative methods are applied to the utilization of primary and secondary data. The Survey research strategy, the most suitable technique for gathering descriptive information, is used in this study. This research technique covered targeting the population and getting the responses in the questionnaire. The target population here covers specifically users and prospective users of E-Banking services. The researchers picked respondents mostly from the Dutch Bangla Bank Limited, Prime Bank Limited, and Bank Asia Limited in the Chattogram. The majority of the respondents are customers, although the questionnaire also took an informal interview with bankers and other experts. Both convenience and purposive sampling techniques were applied for data collection, in this research.

6. b) Data Collection Procedure

With the combination of closed and openended questions, the researchers prepared a structured questionnaire to collect data. As the most versatile method to yield clean data, "Multiple choice questions" applied, and respondents were allowed with optional answer. The questionnaire also contained an additional "other" option with a comment field so that respondents can write down responses that were not available in the given options. Though, different write in responses made the researcher do some extra work about separating each which, helped to get unbiased responses because the respondents were not bound to a fixed number of answering options. There is also the inclusion of some open-ended questions to let respondents provide their suggestions and recommendations.

7. c) Data Processing and Analysis

After assembling and organizing data by the structured questionnaire, the researcher coded, cleaned, and filtered those through Microsoft Excel and Google Analytics. Besides, statistical analysis applied by the software to show alliance among variables, and frequency distribution is used as a statistical analytical method for displaying descriptive statistics. The consistent data has been then manifested in a standard model using tables, frequencies, and percentages to analyze and interpret the data. Besides, the mean/average score is considered in determining the ranking of some multiple answer options. Finally, the results are illustrated by charts and tables for a better understanding of the analysis.

IV.

8. Result and Discussion

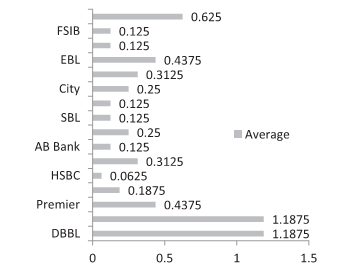

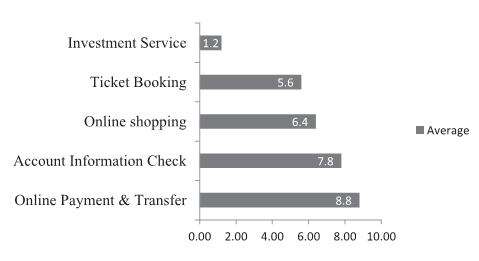

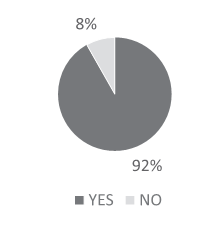

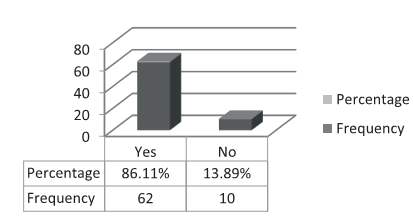

The researchers at first tried to find out customers' bank selection. 88% of respondents unveiled the bank name where they maintain the accounts. Most of the respondents have an account in more than one bank. Therefore, the table is arranged so that we can derive how many times the responses are opted on an individual bank name and their ranking in terms of average score. However, people have mentioned about 16 different banks. Most of the respondents have the account in both IBBL and DBBL; thus, in the table, we Secondly, the researchers aimed at exploring customer's perceptions of different types of service delivery channels. 98% of respondents expressed their preferences. It is visible that most of them responded (43.84%) opted for "Electronic Banking" as their preferred Banking system, which is not up to the expectation. The response on only "Traditional banking" is relatively lower. However, both the banking system option (41.10%) is pretty close compared to the option "Electronic Banking." Thirdly, 68% of the total respondents defined Ebanking in 5 different ways. According to most respondents (29.41%), E-banking is banking with Electronic Media and the inter net. They added that banking services, pro vided through mobile, PC and internet are called E-banking. Whereas (27.45%) of the respondents defined it as "Internet-Based Banking." They think that all types of banking procedure facilitated by the internet are said to be E-Banking. (27.45%) of the respondents understood it as "Online Based Banking. In their view, E-banking refers to the banking system which depends on online activities, and (7.84%) of the respondents referred to e-banking as "Real-Time Banking" which is easy and convenient, time saving and can be operated remotely. Fourthly, the researchers tried to understand what form of e-banking services is mostly demanded in the market. Almost 36% of total respondents prefer the Combination of (Inter-net Banking + Online Banking + Mobile Banking) has a response rate of 28.07%. Be-sides, 24.56% of the respondents chose only "Online Banking" as the form of E-Banking they use.

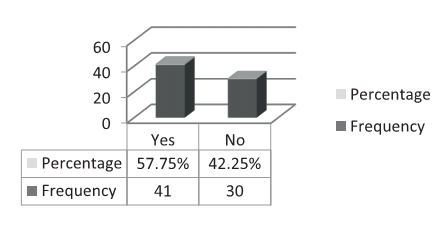

Moreover, the combination of (Internet Banking +Online Banking) and only Mobile Banking have limited demand. Then, there should be rationality for e-banking services. Almost 58% of total respondents find E-Banking facility as efficient and admit the option "ALL" (Convenience, Easy Access, Time Saving, No need to stand in line, Cost saving) for the reasons/advantage of using E-Banking Facility. At the same time, other combinations of choices got the nearer percentage of responses from the respondents. Still, a remarkable section of our population is Not interested in E-Banking services. Majority of the non-interested respondents (55.74%) addressed that they have no clear idea about the security system in ebanking. At the same time, some respondents (19.67%) found as "Lack of Technological knowledge" for their reason for not choosing this service. The combination of "Security Issue and Lack of Technological Knowledge" has 9.84% response, and 6.56% have chosen the option "ALL" as the reason for not choosing E-Banking service. Finally, the researchers checked the customer's recommendation on e-banking services an d patterns. Despite the growth, experts claim that e-banking is still in its infancy in Bangladesh. In this case, maximum respondents (31.25%) recommended that the security should be enriched by ensuring that the computer system is used only by the trusted people, creating a security framework, etc. At the same time, 14.06% of the respondents emphasized the training of both employees and customers. They suggested trained IT experts should be employed, and basic training to be given to the customer by the friendly employees. Ensuring education with technological knowledge is inevitable for the growth of E-banking, 12.50% of the respondents suggested about this. They added that without education level people would be unable to use the internet and operate electronic devices. The same percentage (12.50%) of respondents claimed that E-Banking would be accepted to a larger extend only when it becomes flexible, easy, and convenient to use for all kinds of clients. Moreover, some other recommendations pro vided by the respondents are creating intense awareness about e-banking, especially in a rural area, building a robust infrastructure and regulatory framework, reducing the prices of internet and additional e-banking charges finally, enacting government law such as information security law. V.

9. Global Journal of Management and

10. Global Journal of

11. Conclusion

Digitalization of the banking industry is one of the elements of the "Digital Bangladesh" Vision. The rapid growth of smartphone penetration, and the rise in internet users, will further influence the adoption of E-Banking in our country. In this study, it is evident that the majority of the bank in our country are adopting information technology to render services. The survey focuses that majority of the respondents are concerned about E-Banking. People accept it beneficial in terms of quality, time, access, etc. However, the tendency of the practice is mostly inoperative and sluggish still. Indeed, banks are integrating different E-banking services and features through marketing, advertisement, and raising awareness. Several "Security breaching" events in the banking sector of Bangladesh made people puzzled. Therefore, both the government and the Banks should come forward to save this prospective banking system from the cold static situation by ensuring literacy level, developing infrastructure, enacting a security law framework, creating skilled and trained workforce, and considering the recommendations mentioned in this study. Promoting financial literacy, availability of cheaper network facilities, sufficient ICT infrastructure, and workforce development, strict compliance maintenance, etc., could accelerate E-Banking adaptation more efficiently and satisfactorily. Regulations also need to be active to check money laundering chances through Ebanking platforms.

12. Global Journal of Management and Business Research

Volume XXI Issue I Version I Year 2021 ( ) A

| Most |

| E-Banking Adoption in Bangladesh; Present Status and Customer Satisfaction: An Evaluation | ||||||

| Year 2021 | ||||||

| 54 | ||||||

| Volume XXI Issue I Version I | ||||||

| ) | ||||||

| ( A | ||||||

| Global Journal of Management and Business Research | Types of Bank SOCBs(06) SDBs(02) | No. of ATM (own) 204 0 | No. of ATM' (Shared) 14,753 0 | No. of Total Branches 3,732 1,410 | No. of Branches with online coverage 3,004 70 | % of Online Branches 80.49% 4.96% |

| PCBs(40) | 9763 | 84873 | 4826 | 4825 | 99.98% | |

| FCBs(09) | 168 | 4,207 | 66 | 66 | 100.00% | |

| G. Total | 10,135 | 103,833 | 10,034 | 7,965 | 79.38% | |

| Source: Quarterly Review Report (2017), Bangladesh Bank | ||||||

| Product/Service | No. of bank | % of Bank |

| Internet Banking | 40 | 78.43% |

| Online Banking | 38 | 74.51% |

| Mobile Banking | 41 | 80.39% |

| Automated Teller Machine | 48 | 94.12% |

| Debit Card | 46 | 90.20% |

| Credit Card | 47 | 92.16% |

| Banking System | Frequency | Percent |

| Electronic Bank | 32 | 43.84% |

| Traditional bank | 11 | 15.07% |

| Both | 30 | 41.10% |

| Total | 73 | 100.00% |

| View of E-banking | |

| Electronic Banking | 15.69% |

| Banking with Electronic Me-dia and internet | 29.41% |

| Internet-Based Banking | 27.45% |

| Online Based Banking | 19.61% |

| Real-Time Banking | 7.84% |

| Total | 100% |

| Form of E-Banking | Per-centage |

| ATM + Debit Card +Credit Card | 35.09% |

| Internet Banking + Online Banking + Mobile Banking | 28.07% |

| Online Banking | 24.56% |

| Internet Banking + Online Banking | 10.53% |

| Mobile Banking | 1.75% |

| Total | 100.00% |

| Year 2021 |

| Volume XXI Issue I Version I |

| ) |

| ( A |

| Business Research |

| Disadvantage | |

| No Idea about Security | 55.74% |

| Lack of Technological Knowledge | 19.67% |

| Speed Issue | 1.64% |

| Security Issue and Lack of Technological Knowledge | 9.84% |

| Other | 6.56% |

| All | 6.56% |

| Total | 100.00% |

| E-Banking Adoption in Bangladesh; Present Status and Customer Satisfaction: An Evaluation | |

| Year 2021 | |

| Volume XXI Issue I Version I | Percent |

| ) | |

| ( A | |

| Management and Business Research | |

| © 2021 Global Journals | |

| Occupation/ Profession | Percent |

| Government Service | 12.16% |

| Private Service | 28.38% |

| Business (Me-dium) | 17.57% |

| Self-Employed | 33.78% |

| Housewife | 8.11% |

| Total | 100% |