1. Introduction

ew ideas and innovations foster the economy of a country as a boon. But owing to several factors, this economy becomes paralyzed in supporting new ideas and innovations. Therefore, for the lack of support from the participants of the economy, these ideas get squelched and lose their ability to boost the economy. The primary factor that hinders new ventures is the lack of financial support, whereas financial supporters have their reasons for their attitude towards new venture financing. On the other hand, the intensifying competition among the business houses and the survival possibility of the new ventures within this are snowballing the opportunity cost of startup financing. This overall process puts us in a paradox whereas economy itself is biting short its opportunity. On the backdrop of this scenario, the quest of the researchers of this article is to identify the alternative financing option for the entrepreneurs in Bangladesh, and here we find the solution of this paradox, which is familiar by the name of "Crowdfunding."Crowdfunding is the process of asking the public for donations that can subsidize the need for capital for the startups (Steinberg & DeMaria, 2012). Furthermore, this process is enabled by modern internet technology whereas potential investors are asked or requested by the entrepreneurs for financial assistance through the internet (Steinberg & DeMaria, 2012). "Crowdfunding involves an open call, essentially through the Internet, for the provision of financial resources either in the forms of donations (without rewards) or for something like monetary or nonmonetary rewards and voting rights to support initiatives for specific purposes" (Belleflamme, Lambert, & Schwienbacher, Crowdfunding: Tapping the Right Crowd, 2010). The contributors may become appurtenant as they provide both financial support and valuable insights (Buysere, Gajda, Kleverlaan, & Marom, 2012). Moreover, they may not look for any direct or immediate return from the venture (Buysere, Gajda, Kleverlaan, & Marom, 2012). In developed countries, this source for financing venture capital has been proved successful. But in case of developing countries, the necessity for assessing the context and environment of institutionalizing crowdfunding platform (infoDev, 2013) is addressed on this research. Because, the economic environment of developing countries is different in terms of regulatory framework for financial institutions, technological awareness among stakeholders (i.e., entrepreneurs and investors), transparency and assurance of the financial settlements, etc.

The economy of Bangladesh is growing with GDP growth rate of 7.05%, whereas the inflation rate is only 5.53%, vis-à-vis (Ministry of Finance, 2016; The World Bank, 2016), which is phenomenal. However, the financial market is critical for financing any venture and lack of stability since the capital market crisis in 2010-11. Lack of investor's confidence and transparency, their N gambling attitude, and regulatory flaws were some of the reasons behind the stock market crash on that period (Wahab & Faruq, 2012; Unnayan Onneshan, The Innovators, 2013). Despite the hard struggle of the concerned authorities, some of these problems are appeared to be persistent currently.

In this juxtaposed situation, it is worthy enough to assess the socio-economic environment of Bangladesh to know suitability and feasibility of crowdfunding. For addressing this issue three objectives or expected outcomes are set for this study. First, exploring the regulatory reformations needed to institutionalize crowdfunding in Bangladesh. Second, assessing stakeholder's (i.e., investors and entrepreneurs) bilateral technological readiness for crowdfunding process.

Third, analyzing the determinants of their behavioral intention to participate in CF process.

2. II.

3. Literature Review

Crowdsourcing is considered as the predecessor concept of crowdfunding, whereas crowdfunding only deals with the task of raising fund through internet (Ibrahim & Verliyantina, 2012;Brabham, 2008). In crowdsourcing, different things like ideas, opinions, resources, feedbacks, etc. are obtained from the public (Howe, 2006). At the same way, crowdfunding means collecting or raising money from the crowd in exchange of nothing (this process is known as the donation) or something (reward or return), while an internet-based community platform may work as a mediator (Nesta, 2014). Although this is the old concept started from the very beginning of humans, but now this process is based on modern technologies and new approaches. The crowdfunding process may consist of three parties based on three distinctive roles played by them on the CF process (Cunningham, 2012). These are: (a) entrepreneurs, (b) crowd-funder (a.k.a. sponsor, backer, investor), and (c) crowdfunding platform (a third party or mediator provides online platform, like as Kickstarter, Indiegogo, RocketHub, etc.).

The picture of crowdfunding may be enlightened from the story of the successful crowdfunding campaign ever happened in the history, where Kickstarter (a crowdfunding platform) has raised $10,000,000 (but the initial goal was to collect $100,000) for Eric Migicovsky (Current CEO of Pebble Technology) within six months. So, that is the capability of this platform (Scholz, 2015).

Based on the motivations of the investors crowdfunding can be categorized into four categories of (1) Donation, (2) Equity/Profit Sharing, (3) Pre-selling, and (4) Lending/Loan (infoDev, 2013). On the other hand, based on the crowdfunding platform (an intermediary institution) provider's intention and business type, there are several business models of CF. a. Threshold Pledge Model: pledging to raise a promised amount by the CF platform, though only after reaching the target amount they can get their fees/charges from the fund seekers. Micro-lending Model: collecting fund from the crowd in small amount and returning the money to the crowdlenders after the promised time. b. Investment or Equity Model: offering equity-based CF option for the funders. c. Holding Model: making a subsidiary company invested by each individual crowd-funders. The Club Model: providing community-based fund raising option (infoDev, 2013).

Several studies are available on crowdfunding, but very few have focused the context of Bangladesh. Only, Adhikary & Kutsuna (2015) have excavated the systematic problems of Bangladesh relating to the gaps in financing options for the startups and evaluated crowdfunding as an alternative solution. According to their argument, crowdfunding can fill up these gaps left by other financial institutions (e.g., banks, NBFIs, microcredits, etc.) without replacing the venture capitalists and business angels. At the same logical ground, Rubinton (2011) has compared crowdfunding with investment banking, whereas the investment can take the forms of donation.

However, this paper is the first comprehensive and rigorous study on crowdfunding and its feasibility in the context of Bangladesh. The focal points of other research initiatives conducted worldwide consist of different aspects of CF like the legal feasibility, technological specifications, entrepreneur's or funder's interest and behavioral dynamics, comparison of CF models, economic implications of CF, significance of campaign and communication networks, etc. The following section provides the snapshots of the literary works done in this discipline.

Regarding the structure of crowdfunding process in a developing country, Ibrahim & Verliyantina (2012) have proposed a model for Indonesia. They have used Web-based Platform and Social Networking Sites (i.e., Facebook, Twitter) as the center of the model. This model dictates that entrepreneurs and crowd-funders will use this Web Based Platform and Social Networking Sites for their respective purposes. Another inseparable part of crowdfunding mechanism is the information system because information system is the prime enabler of crowdfunding process. Shaping the user interfaces, platform, software and other hardware specifications as per the need of executing crowdsourcing campaign defines the level of success in a noticeable extent (Leimeister et al., 2009;Feller et al., 2012). These studies have addressed the technical specification and know-how of the participants of crowdfunding platform in Indonesia. But, the necessity to pre-assess the participant's readiness was not accommodated. On the other hand, some of the researchers have studied on the aspects of policy maker's role in CF process and the regulatory obligations, those are deemed to be another critical element for any CF initiative (Zimmerman & Zeitz, 2002;Burkett, 2011). A research work conducted by Sancak (2016) in Turkey shows that the successful implementation of crowdfunding platform in a country depends on regulatory flexibility. But considering the context of Bangladesh, this is not the only issue is going to be addressed in this research work, because the introduction of CF requires much more attention and transformation of the status quo. Turan (2015) has identified that in developed countries security market regulations are being rectified to incorporate the rules of the WEB 3.0 as a supporting tool of CF. His investigation yielded some recommendations for crowdfunding, such as increasing transparency concerning shareholders' rights, having third-party auditor to evaluate the projects, adopting a code of conduct for bringing professionalism in the industry. His recommendations were particularly important for profit-oriented crowdfunding efforts (Pitschner & Pitschner-Finn, 2014). Along with these, Hazen (2012) has analyzed laws and securities for protecting investor's interest in theUSA.

However, Steinberg & DeMaria (2012) believe that the success of crowdfunding is analogous to the psychological satisfaction and motivation of the stakeholders, where effective promotion can contribute on this aspect (Cholakova & Clarysse, 2015). From the empirical evidence, it is noticeable that the success of such models depends on the ways of promoting these. Jegeleviciute & Valenciene (2015) have meticulously portrayed that how developed countries are doing well in crowdfunding because of their promotional campaigns took place before launching crowdfunding. But the worrisome fact is, in developing countries like Bangladesh same approach may not work at the expected level because of the lack of awareness and consciousness among the people (Adhikary & Kutsuna, 2015).

Kraus et al. ( 2016) has adopted the theory of communication which was initially developed by Schulz von Thun (2000) and showed that how communication with the stakeholders plays a vital role as the success factor of crowdfunding. Though, these studies have merely focused on the communication and promotional aspects, but broader than other contemporary analyses.

Lukkarinen et al. (2016) find that pre-determined characteristics (i.e., the minimum amount of investment, campaign duration, financial provisions, etc.) of crowdfunding campaigns and the utilization of private/public networks (i.e., online and offline) for campaign. Artis (2015) has also stated same thing on "Social and Solidarity Finance" model. Similar kinds of models are also suggested in different studies, whereas the personal relationship between entrepreneurs and investors can be beneficial (Burtch, Ghose, & Wattal, 2011;Busenitz et al., 2003;Cardon, Sudek, & Mitteness, 2009;Cornelius, 2006;Dushnitsky, 2009;Gorman, 1989).On the other hand, Belleflamme et al., (2010)argue that personal benefit of the investors is considered while they are making investment decisions, so keeping this on mind entrepreneurs should shape their crowdfunding campaign. Mollick (2014)has proposed that along with communication or promotional campaign, "project quality" (i.e., profitability, duration or sustainability of the project) and "geographic characteristics"(i.e., project objective, project area, target customers) of the project are also significant. Furthermore, Agarwal et al. (2015) show that how the geographic distance between fundlenders and fund-recipients influences investment decisions of the funders. Both online and offline social interaction are emphasized here to makeover this discrepancy.

However, there are also some other studies concentrating on the behavioral traits and interests of both investors and entrepreneurs. Zvilichovsky et al. (2015) have proposed a crowdfunding platform and emphasized its reciprocity role of preserving the interests of both parties (entrepreneur and investor). Belleflamme et al., (2015) have argued from the crowdfunding platform provider's perspective. They have suggested two-sided market (recipient and funder) approach, whereas information asymmetry between both parties can ensure a win-win situation. Zhao et al. (2016) applied "Social Exchange Theory" to examine the factors behind the financing intention of the investors. They found that commitment of the entrepreneurs, perceived risk of investment, and trust factors had a significant impact on the financing intention of the investors. Ryu & Kim (2016) In a report of World Bank, some other aspects are mentioned essential for any crowdfunding framework. This is the only report recommending the necessity to assess the readiness or preparedness level of a country regarding four dimensions (i.e., technology, culture, capital, and regulation), those are essential prerequisites of implementing CF process (infoDev, 2013).But, no research is conducted yet analyzing the probable acceptance of crowdfunding in Bangladesh. Before initializing crowdfunding platform, it isnecessary to know whether the peopleare ready to invovle with CF or not.That is the issue going to be investigated in this study.

4. III.

5. Theoretical Framework & Hypotheses

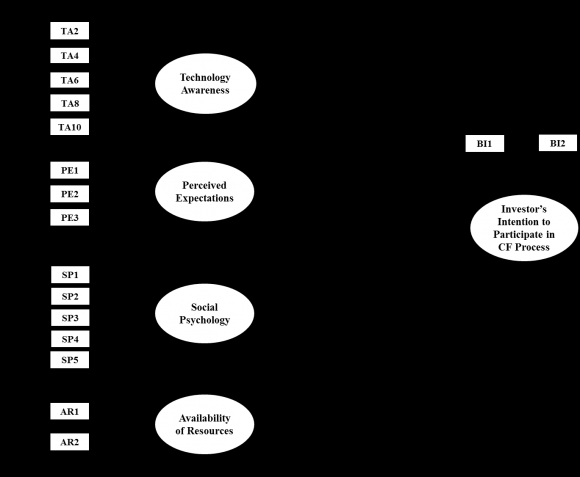

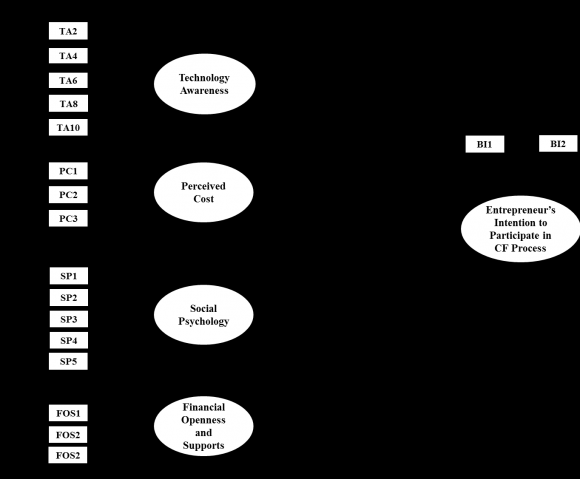

Based on rigorous literature review, variations and insights are found related to the methodological aspects, objectives and the context of the study. The research objectives of this study are formulated by considering these outcomes and the socio-economic condition of Bangladesh. The objectives of this study are to analyze and asses (1) regulatory framework, (2) stakeholder's bilateral technological readiness, and (3) the factors as the determinants of their behavioral intention to participate in CF process. A theoretical framework is developed to represent the 3rd objective and the associated constructs of the study subjected to empirical analysis (See: Figure 1).

6. Technological Awareness

The process of crowdfunding is information and communication technology aided (Zvilichovsky et al., 2015; Majchrzak & Malhotra, 2013), so it is necessary to assess the level of technical know-how of the entrepreneurs and the investors in Bangladesh. The parameters of assessing technological awareness include their access to the smart devices (i.e., smartphone, a personal computer), internet facilities, appearance in social media (e.g., Facebook, Twitter), usage of e-mail service, e-banking, mobile application based services, etc. (infoDev, 2013).

7. Perceived Expectation

Researchers show that vast majority of crowdfunding efforts provides the investors with promised return (Belleflamme et al., 2010;Burtch et al., 2011). Matching between the commitment of the entrepreneurs and the expectations of the investors from the crowdfunded projects is responsible for the success of the projects (Lambert & Schwienbacher, 2010), therefore, it becomes essential to assess investor's perceived expectations (infoDev, 2013).

8. Social Psychology

Social psychology denotes the attitude of the society towards the entrepreneurs, crowdfunding process, trustworthiness to others, partnership business, innovative ideas, profit/loss, risk, etc. (Sajjad et al., 2012;Ajzen, 1991;Bird, 1988;Hayton et al., 2002). Entrepreneur's and investor's perceptions about these socio-psychological issues represent their readiness level required for crowdfunding (Grinbatt & Keloharju, 2001;infoDev, 2013).

9. Perceived Cost

Perceived cost is related to issues like; (a) entrepreneur's opportunity cost related to the decision of accepting crowdfunded capital rather than not selecting other options, (b) the risk of the deterioration of expected project outcome, and (c) failure of CF campaign (Gleasure, 2015).

10. Financial

11. Openness and Support

Entrepreneurs, what are they thinking and perceiving about the fairness of their opportunity to access any financing options provided by the government or any other financing authorities (i.e., Banks, NGOs, Leasing companies, etc.) in Bangladesh.

12. IV. Research Design and Methodology a) Methodological Approach

From the methodological point of view, a mixed approach is applied here. In this study, based on a desk research and literature review the constructs and the variables are determined. On the other hand, causal and conclusive research techniques are applied to test the hypotheses. As it is known that methodological approach represents the plan of a research study containing the issue of how the objectives of a research initiative will be meet (Zikmund et al., 2010;Cooper & Schindler, 2008). Table 3 contains detail about the methodological approach of this study. The target population of this study is the experts including government officials, bankers, and academicians, which is related to the first objective of this study of conducting in-depth interview to identify the regulatory reconciliations and reformations needed to initiate CF process in Bangladesh. On the other hand, regarding the second, third and fourth objectives, the target population are the investors and the entrepreneurs in Bangladesh.

Non-probabilistic sampling techniques (i.e., judgment and snowball sampling techniques) are applied to select the sample units of experts, entrepreneurs, and investors. For conducting an in-depth interview, eighteen experts comprising of five government officials, six bankers, and seven academicians on the related discipline are selected and interviewed by using an open-ended and somewhat unstructured questionnaire (See: Table A1). Along with this, 268 respondents are surveyed based on a structured questionnaire (See: Table A2). After screening, 250 respondent's data (125 entrepreneurs and 125 investors/funders) are used for further analysis. The items of the structured questionnaire represent 31 variables used to measure the 8 readiness factors (See Figure 1 and Appendix: 2). Most of the variables are measured in a five-point Likert scale (1-Strongly agree, 2-Agree, 3-Neutral, 4-Disagree, and 5-Strongly disagree) and the few are measured in nominal scale generating categorical/binary (Yes/No) response patterns. In PLS-SEM analysis, the variables measured in Likert scale are only used. Data were collected by field survey conducted in Dhaka city, which was carried by 25 field enumerators, those were trained before data collection.

13. Findings, Interpretations, and Implications

Three issues are analyzed, interpreted, and addressed here. These are: (1) What are the regulatory compliance and reformations needed to institutionalize crowdfunding in Bangladesh based literature review and in-depth interview? (2) Do the entrepreneurs and investors have enough technological readinessto participate in crowdfunding? (3) What are the factors determining their behavioral intention to participate in a crowdfunded project? a) Regulatory and Legal Feasibility of Crowdfunding in Bangladesh

Crowdfunding is not a new concept throughout the world, but recently it is brought under some specific rules and regulations to monitor the processes related to this. Likewise, on October 23, 2013, the Securities and Exchange Commission of USA implemented the "Jumpstart Our Business Startups" Act (a.k.a. the JOBS Act) for legally supporting the CF processes (kelleydrye.com, 2013). On November 16, 2015, they also approved the new regulations and permitted companies to offer and sell their securities through authorized crowdfunding platforms in reliance on the exemption under Section 4(a)(6) of the Securities Act of 1933 (Tate, 2015).

But in Bangladesh, there is no such legal framework for controlling and regulating crowdfunding process. In the backdrop of this fact, a few crowdfunding platforms are initiated here in Bangladesh till now. Some crowdfunded projects are implemented with the help of the platforms like Kickstarter, crowdfunder.co.uk, StartSomeGood.com, etc. "Project Aim at Sreepur Village," "Tripty Project: Ethically Made in Bangladesh," and "Positive Light" are some of the examples of crowd-funded projects ever happened in Bangladesh, those were non-profit oriented (kickstarter, 2016; whydev, 2012). A self-motivated entrepreneur Waiz Rahim has introduced the first local CF platform named as "project.com" in Bangladesh (Reaz, 2015). dog without a master. Based on the in-depth interview, it is anticipated that whenever CF is going to take place here in a broader way, but it will be messy without any legal and regulatory frame. So, the experts think that this is the right time to formulate customized rules and regulations for CF in Bangladesh which will ensure the maximum interest of entrepreneurs and also the safety of investors. On the other hand, as we know that the people here in Bangladesh have gone through some unfortunate financial fraudulent experience such as Destiny2000 limited, unipay2u, stock market crash, etc. in the recent past and these activities can be attributed to the deficiency and loopholes of the legal framework. So, expert's opinions are suggesting that having legal boundaries will prevent similar fraudulent event likely to arise from crowdfunding.

There are certain types of financial instruments available in Bangladesh those are like crowdfunding, mutual fund schemes, for instance. Crowdfunding is like this regarding the collection of the fund, amount of subscription, and underlying. But the usage of the fund is different from each other. Fund collection mechanisms and the concerned law of mutual fund depicted in Securities and Exchange Commission Rules of 2001 can be utilized in preparing a regulatory framework for CF. Along with this; we can also use Investors' Fund Protection Regulations of 1999 to keep them safe from being betrayed. Crowdfunding is new and tech-savvy than any other traditional financial instruments. To create a legal framework covering these aspects, we can also follow the newly approved Regulatory Framework of USA. Following points give a very brief idea about this law (kelleydrye.com, 2013):

? Eligible companies can raise the maximum amount of $12 million on a 12-month rolling basis. ? Investors will not need to meet any wealth thresholds, but they will have a limit on the amount of investment made in 12 months. ? Crowdfunded offerings will need to be conducted through a registered broker or a registered funding portal. ? Crowdfunding will be restricted to online-only platforms. ? Before crowdfunding offering the issuer must disclose all the facts of the projects and that substantial information should be audited by independent audit firms. ? After the successful offering of crowdfunding, the issuer will be required to submit annual reports to the SEC until it becomes a public limited company. These basic rules can be implemented in any country given the infrastructural support. The regulatory authorities of Bangladesh such as the Bangladesh Bank, Securities and Exchange Commission, Registrar of Joint Stock Companies, Ministry of Finance, etc. should be coordinated. With their regulatory support, a legal framework can be created for the future crowdfunding initiative. It will not only create a safe and sound environment for the entrepreneurs and investors but also inspire them to go for such initiatives as they will have a fixed path to follow. b) Demographic Characteristics and Readiness of the Stakeholders i. Demographic Features of the Respondents Demographic data(See: TableA3) of the respondents (investors and entrepreneurs) show that most of the entrepreneurs (total 83%) are belonging to the age groups of 21-30 and 31-40 when the investors are from 41-50 and 51-40 (total 65%). There is also a significant difference between investors and entrepreneurs regarding their education level and profession. 36% of the entrepreneurs are not involved with any other job, and 22% are having their own business. On the contrary, 45% investors are businessmen. The surprising part is the lack of gender diversity, but women entrepreneurs and investors should be encouraged and patronized to come forward to contribute to the socio-economic development and CF process in Bangladesh.

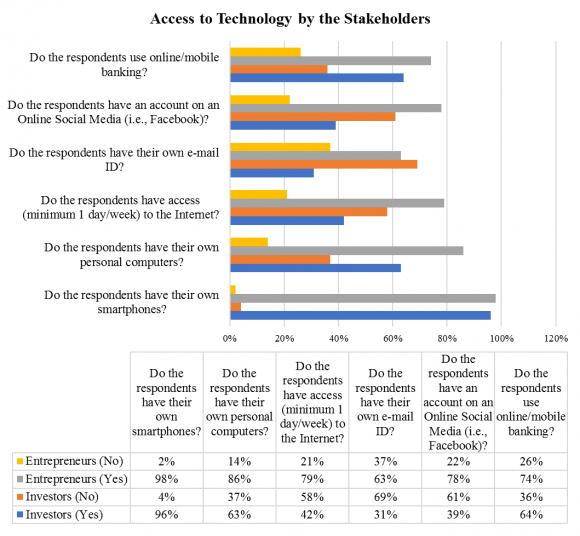

14. ii. Bilateral Technological Readiness of the Respondents

On the other hand, significant differences are observed (See: Dashboard 1) between the investors and entrepreneurs in accessing and using modern technologies and technology-aided services in Bangladesh. Such as, the usage of smartphone, personal computers, Internet, social media (e.g., Facebook), e-mail services, online/mobile banking, etc. As it is observed that 79% entrepreneurs have internet access, where 58% of the investors are not continuously connected to the Internet. It may cause a significant impact on the usage and acceptance of CF process by them.

However, Dashboard1contains the actual scenario related to the technological readiness level of the investors and entrepreneurs towards crowdfunding as a new initiative in Bangladesh. Bilateral technological readiness is measured by five indicators (See the observed variables 2, 4, 6, and 10 of the construct of "Technology Awareness" from Appendix A2), whereas the responses against each indicator were collected in a 5-point Likert scale. For the sake of simplicity, responses are grouped into three categories. These are:

(1) Favorable to CF Process ("Strongly Agree" and "Agree" in the Likert scale), (2) Probable Favorableto CF Process ("Neutral" in the Likert scale), and (3) Unfavorable to CF Process ("Disagree" and "Strongly Disagree" in the Likert scale). It is obvious that, technologically, entrepreneurs are more prepared to accept crowdfunding in Bangladesh rather than the investors. Based on these facts, two suggestions can be derived for the potential CF platform providers; (1) "Snatching the Opportunity" -those are in favor of CF can be capitalized to do business with them as an intermediary; (2) "Grooming-up them" -those are in neutral and unfavorable position can be motivated and trained up to transform them into favorable participants. The findings of this analysis bring a lot of insights about the potential business model of crowdfunding platform and prerequisite context of crowdfunding in Bangladesh. The findings of this study can be applied to realize -what are the factors should be considered and how much will it be successful if anyone goes for initiating crowdfunding in Bangladesh. These will help them to develop rigorous action plan associated with crowdfunding. Table 4 contains the threshold values used to compare with the estimated values depicted in figure 2 and 3. Based on the Table 4, and Figure 2 and 3 following inference can be derived regarding the hypotheses of this study.

15. Global

16. Limitations

The primary limitation of this study is related to two aspects. One is the research area, and another is the demographic impact on the findings. This study is mainly conducted in Dhaka city due to the time and resource limitations; which may not be an ideal represent of the rural scenario. On the other hand, demographic characteristics of the respondents may have the mediating or moderating effect on the outcomes derived by PLS-SEM analysis.

17. VII.

18. Conclusion

The findings of this study will be helpful enough for the policy makers, government, corporate bodies, CF platform initiators, investors, entrepreneurs, and NGOs. This study is carrying a clear and comprehensive picture of the status of the pre-requisite context of crowdfunding. The initiative of institutionalizing crowdfunding process in Bangladesh as an alternative source of long-term finance for the startups or new ventures may follow the findings of this study. Crowdfunding can be the most promising source of finance and may be a strong alternative to other financial intermediaries in Bangladesh. This study is conducted by realizing this fact and for fostering the pace of CF.

| H1: | "Technology Awareness" significantly affects "Investor's Behavioral Intention to Participate in CF Process." |

| H2: | "Perceived Expectation" significantly affects "Investor's Behavioral Intention to Participate in CF Process." |

| H3: | "Social Psychology" significantly affects "Investor's Behavioral Intention to Participate in CF Process." |

| H4: | "Availability of Resources" significantly affects "Investor's Behavioral Intention to Participate on CF Process." |

| H5: | "Technology Awareness" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." |

| H6: | "Perceived Cost" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." |

| H7: | "Social Psychology" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." |

| H8: | "Financial Openness & Supports" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." |

| Objectives of the Study | Data Collection Techniques | Data Analysis Tools | Nature of Analysis | |

| 1 | Exploring and identifying the regulatory compliance and reformations needed to institutionalize crowdfunding in Bangladesh. | In-depth Interview with the Experts | Descriptive or Desk Research | Qualitative |

| 2 | Assessing stakeholder's (i.e., investors and entrepreneurs) bilateral technological readiness. | Structured Questionnaire based Field Survey | Descriptive Statistical Tools | Quantitative |

| Analyzing the determinants of stakeholder's | Structured | Partial Least Square- | ||

| 3 | behavioral intention to participate in the | Questionnaire based | Structural Equation | Quantitative |

| crowdfunding process. | Field Survey | Modelling (PLS-SEM) | ||

| V. |

| li | Factor/Outer Loadings of the indicators to their respective constructs (More than 0.708 is considered as statistically significant) |

| IR (Indicator reliability) is the squared values of the loadings representing the amount of variance in | |

| IRi | the indicator variables explained by the corresponding constructs in a reflective measurement |

| model (value more that 50% is significant) | |

| ?c | Composite Reliability is calculated to assess the internal consistency of the measurement model (values from 0.70 to 0.90 are considered statistically significant) |

| ? | Cronbach's Alpha is as much as like composite reliability used for the same purpose (values from 0.70 to 0.90 is acceptable) |

| AVE | AVE (Average Variance Extracted) is equal to the summations of Iris divided by the number of indicators (values from 0.70 to 0.90 is acceptable) |

| f2 | f2 (Effect size) denotes the contribution of the exogenous constructs in the R2 value of the endogenous construct (value>0.35 represents strong effect) |

| Q2 | It means the predictive relevance of the independent constructs over the dependent construct (value>0.35 represents strong effect) |

| FL= | FL (Fornell-Larcker Criterion) represents discriminant validity of the measurement model (FL value |

| ?AVE | of a construct > correlation with any other constructs is acceptable) |

| VIF | VIF (Variance Inflation Factor) represents the degree of multicollinearity among the exogenous constructs (values < 5 denotes no multicollinearity) |

| ? | Path Coefficients among the constructs (Acceptable if it is significant at 1%, 5%, or 10% level of significance) |

| t | Calculated value of t-statistic which is compared with the critical value of 2.52 (at 1%), 1.96 (at 5%), and 1.64 (at 10%) |

| R2 | Coefficient of Determination denotes the degree of variance in the dependent construct explained by the independent constructs (value > 0.50 is acceptable) |

| H1: | "Technology Awareness" significantly affects "Investor's Behavioral Intention to Participate in CF Process." | Accepted |

| H2: | "Perceived Expectation" significantly affects "Investor's Behavioral Intention to Participate in CF Process." | Accepted |

| H3: | "Social Psychology" significantly affects "Investor's Behavioral Intention to Participate in CF Process." | Accepted |

| H4: | "Availability of Resources" significantly affects "Investor's Behavioral Intention to Participate on CF Process." | Accepted |

| H5: | "Technology Awareness" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." | Accepted |

| H6: | "Perceived Cost" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." | Accepted |

| H7: | "Social Psychology" significantly affects "Entrepreneur's Behavioral Intention to Participate in CF Process." | Not Accepted |

| H8: |

| Strongly Agree-Disagree | ||||

| (5-point Likert scale) | ||||

| 19 | PE3 | My motivation to invest in a project is to maximize my return on investment | Strongly Agree-Disagree (5-point Likert scale) | |

| Perceived Cost (Respondents: Entrepreneurs) | ||||

| 20 | PC1 | I think my project will not always be in a profitable condition. | Strongly Agree-Disagree (5-point Likert scale) | |

| 21 | PC2 | I think that investors are going to only focus on their financial returns/benefits | Strongly Agree-Disagree (5-point Likert scale) | |

| 22 | PC3 | I think the opportunity cost of accepting investment from individuals will be higher than other institutional options | Strongly Agree-Disagree (5-point Likert scale) | |

| 23 24 | AR1 AR2 | Availability of Resources (Respondents: Investors) I think I have enough savings to invest in any innovative projects I think I can bear the risk of lending money to others | Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) | 2018 Year |

| Financial Openness and Supports (Respondents: Entrepreneurs) | ||||

| 25 FOS1 26 FOS2 27 FOS3 28 BII1 29 BII2 30 BIE1 31 BIE2 | In Bangladesh government is doing well in terms of helping entrepreneurs Entrepreneurs are getting enough supports from financial institutions In Bangladesh, different NGOs are working in favor of the entrepreneurs Behavioral Intention of the Investors I think CF is an effective way to help entrepreneurs I think I can invest through CF process in Bangladesh Behavioral Intention of the Investors I think CF is an effective way to get financial assistance from others I think I can raise capital through CF process for my new venture | Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) Strongly Agree-Disagree (5-point Likert scale) | Global Journal of Management and Business Research Volume XVIII Issue I Version I C ( ) | |

| Entrepreneurs | Investors | Entrepreneurs | Investors | ||

| Age | Education Level | ||||

| Less than 21 | 6% | 0% | Primary | 0% | 6% |

| 21-30 | 54% | 5% | Secondary | 0% | 17% |

| 31-40 | 29% | 18% | Higher Secondary | 10% | 30% |

| 41-50 | 9% | 37% | Graduation | 21% | 19% |

| 51-60 | 2% | 28% | Post-graduation | 54% | 22% |

| More than 60 | 0% | 12% | Vocational/Technical Education | 15% | 7% |

| Gender | Profession | ||||

| Male | 98% | 100% Business | 22% | 45% | |

| Female | 2% | 0% | Private Job | 31% | 24% |

| Public Job | 10% | 31% | |||

| Unemployed | 36% | 0% | |||