1. Introduction

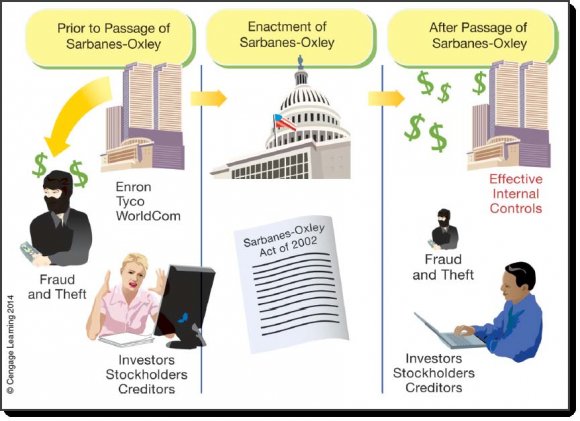

his research paper will introduce seven parts in the literature review as it relates to the collapse of Enron Corporation. The three major violations under Generally Accepted Accounting Principles (GAAP) that preceded the fall of the Enron Corporation were: (1). The off-balance sheet arrangements, (2). The role of mark-to-market, and (3). The manipulation of derivatives. In 1977 the United States Congress passed the Foreign Corrupt Practices Act (FCPA) to prevent major financial irregularities in the market such as corporate bribery, violation of an accounting system, and so forth. By the mid-1980s, the United States Government committed to examine all failures and fraud in the financial market. However, in 2002 the United States Congress passed the Sarbanes-Oxley Act of 2002 to prevent accounting scandals such as Enron, Arthur Ardersen, and Tyco. The purpose of the act was to reestablish the financial trust and confidence of investors among major publicly traded companies in the United States market (Warren, Reeve, & Duchac, 2014).

The United States Securities and Exchange Commission (SEC), after adopting the Sarbanes-Oxley Act of 2002, introduced 11 chapters or provisions by reshaping the accounting system and designing unique sets of rules and regulations. Section 404 under the Sarbanes-Oxley Act of 2002 requires management and independent auditors to report their findings with accuracy and reliability in the unqualified opinion report. Since the implementation of the Sarbanes-Oxley Act of 2002 information technology (IT) has provided high relevancy and compliance in the accounting industry. Also, the types of services that are considered unlawful are price fixing, inappropriate use of the tax law practices for money laundering off-shore, and violation of the laws and social norms in society. Consequently, the prohibitions set by Sarbanes-Oxley (SOX) impacted not only the auditors but also professional accountants.

2. II.

3. Literature Review a) The Historical Background of the Enron Scandal

In corporate American history the most famous corporation to use creative accounting was the Enron Corporation. In 1985 the Enron Corporation was created by the acquisition and merger of two natural gas companies. The Enron Corporation began to expand its line of operations and services in different sectors and as a result acquired utility plants in Brazil, India, the United States, and most importantly the United Kingdom by taking advantage of the deregulated market in the natural gas and electricity industry. For example, Enron Corporation, from a simple energy trading strategy, decided to shift financial directions to trade weather derivatives. Then in 1999 the internet-based trading platform was introduced which gave the Enron Corporation more leverage to trade internet in metals, energy, and woods products. By 2000 the Enron Corporation was the seventh largest corporation by growth revenue in the gas and utility market in the United States territory; however, by October, 2001 the Enron Corporation began to experience financial difficulties which caught investors, who were unaware of Enron's financial strategy manipulation, by surprise. Consequently, on December 2, 2001 the Enron Corporation decided to file bankruptcy. The unprecedented financial events of the Enron T Corporation provided proof that major organizations in the gas and utility industry could fully manipulate a firm's financial statements (Madura, 2015).

4. PART I-Enron's Three Major Violations under Generally Accepted Accounting Principles (GAAP) b) Enron's Off-Balance Sheet Method

The three major violations under Generally Accepted Accounting Principles (GAAP) that preceded the collapse of the Enron Corporation were: (1). The offbalance sheet arrangements, (2). The role of mark-tomarket, and (3). The manipulation of derivatives. The creation of the off-balance sheet method (OBSEs) served its specific purpose in Enron's corporate accounting scandal. In addition, the specific purpose of the Enron Corporation (as cited in e.g., Anson 1999; Evans, 1996) was to increase financial flexibility, decrease the cost of borrowing from creditors, reduce the tax portion, maximize profitability, and adequately improve the financial health of the company as noted by (Angbazo, 1997;James, 1989;Shevlin, 1987). Moreover, the legitimate financial purpose of Enron's utilization of the off-balance sheet was to hide losses and debt from auditors, investors, financial analysts, and regulators. Furthermore, in November, 2001, the Enron Corporation announced plans to consolidate the financial statements by restating $586 million in earnings prior to the period by following the accounting principles of hiding losses and debt under the applicability of the off-balance sheet method as mentioned in the research work of (Kahn, 2002;Henry, 2002). The Wall Street Journal then published seven negative articles concerning the way Enron Corporation was using the off-balance sheet method. Therefore, the Enron Corporation's failure to disclose billions of dollars in debt held by the off-balance sheets (OBSEs) prompted auditors to require additional disclosure in the financial statements (Chandra, Ettredge, & Stone, 2006).

5. c) Enron's Mark-to-Market Method

The mark-to-market method and the special purpose entity were important to the Enron Corporation as an accounting fraud principle. Additionally, the Enron Corporation was subject to external governance because Enron had to report to organizations such as government regulators, private entities, audit analysts in the equity sector, and some other agencies. Moreover, Jeffrey Skilling and Andrew Fastow were the pioneers in adopting the mark-to-market method in the Enron Corporation by pumping up the stock price and covering major losses while continuing to attract major capital investment, which was both illegal and immoral. As a result, the U.S. Securities and Exchange Commission (SEC) allowed the Enron Corporation to use the mark-to-market accounting method. For example, Enron's unrealized gains (as cited in Thomas, 2002) were $1.41 billion reported as a pretax profit in 2000 and one-third was reported as a pretax profit in 1999. Therefore, one of the major causes of Enron's fall was the U.S. Securities and Exchange Commission (SEC) allowing Enron Corporation to use at best capacity the mark-to-market accounting method (Li, 2010).

6. d) Enron's Derivatives Manipulation

The third major violation of the Enron Corporation under Generally Accepted Accounting Principles (GAAP) was the manipulation of derivatives which increased from $1.8 billion to $10.5 billion. The management team of Enron utilized specific financial tactics to hide losses in the derivative section; furthermore, investment and commercial banks advised investors about the underwriting problem at Enron. For example, the three most important credit agencies known as Moody's, Standard & Poor's, and Fitch/IBC failed to disclose the financial trouble at Enron because Enron paid the three credit agencies substantial monies by not properly advising the investors at Enron of such existing financial problems. Another example, ESM Government Securities created large receivable fraud by hiding $400 million in the balance sheet. Therefore, the law firms that represented Enron made a big profit from derivatives contract (Albrecht, Albrecht, Dolan, & Malagueno, 2008).

Derivatives are complex financial contracts that are represented under (1) price of commodities, (2) stocks, and (3) bonds. In addition, the derivatives were managed by sophisticated investors in the market and the manipulation occurred internally and externally on Enron's organizational environment by trading big portions of revenues. For example, in 2000, Enron reported more than $16 billion in gain from derivatives. Additionally, since 1997, Enron traders had planned out the manipulation of derivatives in the utility financial market industry with the intent to hide losses ("Derivatives," 2002).

7. PART II -The Purpose of the Sarbanes-Oxley Act of 2002

The purpose of the Sarbanes-Oxley Act of 2002, which was passed by the United States Congress, was to reestablish the financial confidence of stockholders, creditors, and other investors that lost billions of dollars in the market. The main purpose of the United States government passing the bill was to create confidence and financial trust among major publicly traded companies in the market. Furthermore, the Sarbanes-Oxley Act of 2002 expressed the importance of assessing the financial reports of all companies. As a result, Sarbanes-Oxley Act of 2002 promulgates three important internal control processes which are (1). Safeguard the assets, (2). The information must be processed accurately, and (3). Comply with the laws and regulations. Therefore, this act requires publicly Title II -Grant authority to the auditors' to be independent from the company that the auditors are auditing. The main objective of this title is to avoid financial incentive to auditors.

Title III -The audit committee must be composed of independent members. For example, Section 302 under the Sarbanes-Oxley Act of 2002 requires CEOs and CFOs to revise financial statements on a quarterly and yearly basis, otherwise penalties would apply such as a fine of $5 million or up to 20 years in prison because of misleading financial information on the financial statements. Also, Section 304 under the Sarbanes-Oxley Act of 2002 deals with an executive's reimbursement equity capital.

Title IV -Indicate the importance of understanding Sections 401, 404, and 409. As a result, Section 401 deals directly with the disclosure on off-balance sheet transactions. Section 404 in this section evaluates the internal control system of the financial statements by following management's principles. Section 409 requires the company to disclose any material changes in the financial statements and, as well, prohibits the number of loans that can be extended to executives. Title V -Deals with the existing relationship between the financial analyst and investment banks requiring the disclosure of any conflict of interest in the stocks recommended.

Title VI and VII -Deals with the technical budgetary aspect of the SEC. Title VIII -A whistle-blower reporting fraudulent activities is protected under this title and anyone destroying an audit record will face severe legal consequences and penalties for lying.

Title IX -Deals with white-collar crimes and Section 902 initiates the enforcement investigation process of the same. Title X -The CEO is accountable for signing the company's federal income tax return. Title XI -If directors from a company are obstructing the investigation, the SEC has full authority to remove them from their current position if the directors committed fraud.

The U.S. Securities and Exchange Commission (SEC), after the adoption of the Sarbanes-Oxley Act of 2002, introduced 11 chapters or provisions by reshaping the accounting system and by designing a unique set of rules and regulations. In addition, the main objective of the U.S. Securities and Exchange Commission (SEC), with the adoption of the 11 chapters or provisions, essentially mandated companies to have their financial books audited by independent auditors by providing explicit responsibility and governance in terms of financial reliability and accuracy within the organization. Moreover, the independent auditor opinion must be reliable and fairly evaluated by not violating the rules under generally accepted accounting principles (GAAP). Furthermore, investors and other users of the financial statements can feel confident about the independent audit conducted by the auditors. Therefore, the 11 chapters or provisions under the Sarbanes-Oxley Act of 2002 reshaped the sustainability of financial reporting valuation analysis in the accounting industry (Wahlen, Baginski, & Bradshaw, 2015).

8. PART IV -The Requirements Concerning Internal Controls for Public Companies

Section 404 under the Sarbanes-Oxley Act of 2002 requires management and independent auditors to report their findings with accuracy and reliability. In addition, regulators and publicly traded companies (as cited in Baldwin and Yoo, 2005, GAO, 2006, Grothe, Pham and Saban, 2006, Grothe, Goodwin, Iandera, Laurion and Freeland, 2007a, Grothe, Saban, Plachecki, Lee and Post, 2007b, Audit Analytics, 2007, PCAOB, 2007) have devoted sufficient time to studying the sustainability of section 404. Moreover, Section 404's internal control system (as cited in Plumlee, & Yohn, 2010) is likely expected to improve the financial reporting system by utilizing three accounting measurements which are (1). Examine the internal control weakness within the company, (2). Specify the type of internal control problem, and ( 3). Indicate the number of deficiencies by suggesting the impact in the financial restatements. However, Section 404 under the Sarbanes-Oxley Act of 2002 (as cited in PCAOB, 2004) offers an unparalleled effective internal control system. For instance, the internal accounting control system of Section 404 helps to prevent poor financial reporting and most importantly detects fraud. As a result, there is an existing relationship between the internal accounting control system and financial restatement because once a company restates the earnings the material weakness should be disclosed properly in the financial records. Therefore, empirical research studies suggest (as cited in Grothe, Goodwin, Iandera, Laurion and Freeland (2007a) and Grothe, Saban, Plachecki, Lee and Post (2007b), when an auditor is examining the internal accounting control system of a company he or she needs to analyze the firm's internal accounting system problem, specify the nature of the internal existing problem, and examine the relationship between the internal control weakness and financial restatements (Wang, 2013).

The seventh largest corporation in the United States was the Enron Corporation that misguided its shareholders by reporting $74 billion which $43 billion was detected as fraud. In addition, the internal accounting control system of the Enron Corporation still is a controversial financial subject. Moreover, Enron's poor internal accounting control system was guided by insufficient accounting resources which attributed to several financial outcomes and which are (1).Poor policies of revenue recognition, (2).Not appropriate segregation of accounting duties, (3).The lack of financial reporting policies and process, and (4).The inappropriate method of reconciling Enron's bank account. Furthermore, it is argued that after the fall of Enron the compliance costs of internal control systems with the largest auditing firm have increased over time. The SOX cost of a compliance internal control system is $3.5 million. In audit fees, Varian's reported in 2010 $51.1 million. The market of an average capitalization of sample companies is $6.4 billion. However, the market capitalization of Apple Inc. in 2011 was $354.4 billion. Therefore, in order to have a solid internal accounting control system a company needs to invest in resources by hiring more talented employees, qualified internal auditors, and consultants (Peary, Karim, Suh, Strickland, & Carter, 2013).

The main objectives of a strong internal control system is to (1) safeguard the company's assets, (2) report accurate business information, and (3) comply with the law and regulations of generally accepted accounting principles (GAAP). In addition, since the fraudulent event of the Enron Corporation, employee fraud has been one of the top priorities in the publicly traded companies internal accounting control system. Moreover, according to the association of fraud examiners $2.9 trillion is lost on employee fraud. Furthermore, accurate financial reporting matters to private and publicly traded companies because businesses must comply with existing rules and regulations and comply with financial reporting standards. For example, researchers suggest five important elements on the internal control system and these are "(1) control environment, (2) risk assessment, (3) control procedures, (4) monitoring, and (5) information and communication" (Warren, Reeve, & Duchac, 2014, p.362 & 363). On the other hand, the limitations of the internal control system are to (1) control the human elements, and (2) recognize the internal cost process by exceeding its benefits. Therefore, an internal control system is sustain by three elements (1).Risk assessment, (2) According to Muglia (2013), as an organization continues to experience rapid growth in the financial market, the information technology (IT) team should test and control the company's internal control system. The researcher suggests five applicable steps concerning internal control systems when complying with the Sarbanes-Oxley Act of 2002. The first step, review and test the applicable information system. The second step, the internal auditor understands the organization's corporate governance and information technology (IT) compliance rules with Sarbanes-Oxley (SOX). The third step, revises the control system narratives. The fourth step consists in analyzing Sarbanes-Oxley (SOX) tools.

The fifth step assesses the control formality of IT testing. Therefore, the five steps mentioned previously will help the internal and external auditors to follow the information technology (IT) guidance of Sarbanes-Oxley (SOX) (Muglia, 2013).

PART VI -The Types of Services Considered Unlawful if provided to a Publicly Held Company by its Auditors

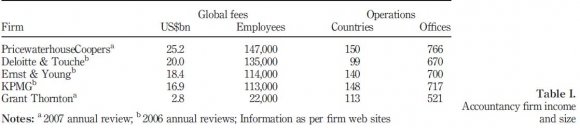

The types of services considered unlawful are price fixing, inappropriate use of the tax law practices of money laundering off-shore, and violation of the laws and social norms in society. In addition, the world of accounting is dominated by four top accounting firms and represents a combined income of $80 billion. For example, the table shows the existing relationship between global fees and operations. four accounting firms as indicated in the previous graph (Sikka, 2008).

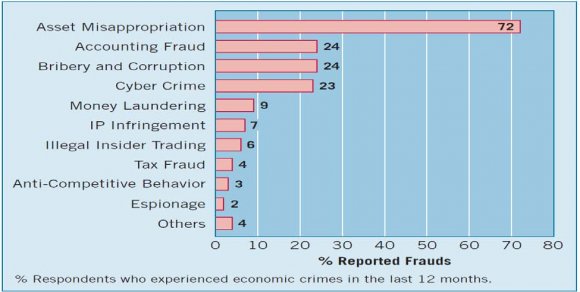

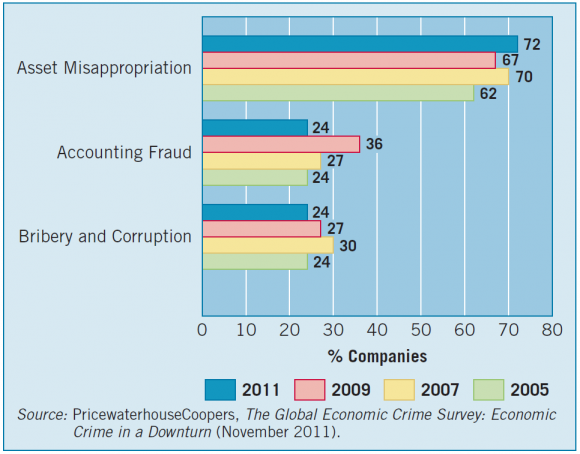

The rapid pace of economic crime continues to strengthen around the globe. As predicated by Kieso, Weygandt, and Warfield (2013), in a global survey study that was conducted in 2013 it was reported that 3,000 executives from 54 countries were involved in fraudulent financial reporting. The graphs depicted below show the results of specific areas of fraudulent financial reporting and the reported fraud trends.

9. Global Journal of Management and Business Research

10. Conclusion

In conclusion, the unprecedented financial event of the Enron Corporation demonstrated that major corporate organizations in the gas and utility industry were manipulating the company's financial statements. In addition, the implementation of the Sarbanes-Oxley Act of 2002 helped align and reshape publicly traded companies financial reporting systems. Moreover, the U.S. Securities and Exchange Commission (SEC) required publicly traded companies with a flow capital of $75 million to comply with the Sarbanes-Oxley Act of 2002. Furthermore, the SOX cost of compliance internal control system is $3.5 million. Therefore, since the adoption of the Sarbanes-Oxley Act of 2002, auditors and publicly traded companies have experienced a high cost of compliance in the financial market among economies of scale. Recommendation for Future Studies

The author of this article suggests that the following aspects should be considered for future studies when examining the collapse of the Enron Corporation: 1. Educators in the higher education arena specialized in accounting studies should align in their course core curriculum the ethical aspect of the 11 provisions of the Sarbanes-Oxley Act of 2002 and the interpretation of corporate governance.