1. Introduction a) Microfinance Market in Turkey

In comparison to neighbouring countries in the South-Eastern Europe and Central Asia, Turkey remains far from reaching its microfinance potential. (2) Despite being the biggest economy of the region with a high number of people unable to access banking services through the formal sector (Burritt, 2003), microcredit schemes are rather new in Turkey and only few research studies were undertaken in this field. (4) Turkey is in acute need of microfinance. Statal social policies developed to help those who receive aid within the aid system to become producers have proved insufficient.(3) According to OECD Factbook, Turkey belonged to the countries with the worst income distribution among OECD members in 2010, being 29th in terms of inequality, with the Gini coefficient of 0.43. The same rank hold Turkey in the category of poverty, with 18.08% of the population living under poverty line. (3) Not with standing the fact that microfinance belongs to the recommended instruments for poverty eradication in Turkey, the sector is in its early stage of development in terms of number of people served as well as of range of services offered. (1) The potential of microfinance appears considerable, giving the fact that SMEs account for 99% of all enterprises in Turkey estimated by TAC 3 In particular microfinance ought to become an empowering platform for a country with low rate of women participating in the labor force, which constitutes another questionmark related to Turkey in relation to microfinance. Suprisingly, significant structural and social changes of recent decades did not facilitate more women to enter the labor markets, although women are becoming more educated, getting married at a later age and the social attitutes toward working spouses has at 4 million units, with non agricultural SMEs employing more than 40% of the workforce, and producing 35% of exports. Access to microfinance would help to decrease vulnerability by enabling microenterprises to take advantage of opportunities, to diversify and to increase sources of income. (11) 2 Gecekondu is a Turkish word meaning a house put up quickly without proper permissions. The gecekondu phenomenon is linked with the problems of unemployment and poverty, especially in the east of the country. 3 Tradesmen and Artisans Confederation microfinance markets in the world. Despite its enormous dormant potential, few studies were undertaken in order to potrait the socio-economic character of its main protagonist: enterprising mother operating in the suburbs of urban and semi-urban environment. The study summarizes result of field research carried out by team of researchers from Czech University of Life Sciences and models a credit mannequin, profiling the average Turkish microfinance client in suburban areas of Central Anatolia. The assemblage enables to depict genuine relationships of mainstream clientele towards selected topics, reaching better understanding of nature and particularities of the Turkish microfinance market and drawing conclusions on its further development.

Substantial disparities of income betwen urban and rural environment persist. Sweeping urbanisation increases the interconnected challenges of infrastructure, labour supply, healthcare, education and security. Moreover, urbanization without adequate collateral development forms a particular type of markets, escalating due to absence of formal property titles in "gecekondu" 1 neighbourhoods, leading to formation of informal job markets conformed by unemployed labourers streaming into urbs from the provinces. Microfinance could play important role by reducing migration pressures consisting in stimulation of economic growth and job creation, both in urban and rural settlements. changed, while fertility rates are declining. Despite these factors, the share of women seeking or having jobs is on the opposite trend than occurring among OECD countries. ( 13 initiatives and stateowned Halk Bank and Ziraat Bank, providing individual loans to SMEs with average loan sum higher than 1,000 USD, the main providers of classical microcredit in Turkey are currently two MFIs, Maya and TGMP, serving loans mostly to female microentrepreneurs operating in the informal sector, with average loan size of about 350 USD. (3) In June 2003, the Foundation for Waste Reduction launched the Turkish Grameen Microfinance Project (TGMP) which applies the Grameen village bank microcredit methodologies of loans to poor people without collateral. TGMP became principal partner for the survey project being a prime Turkish MFI with substantial experience gathered, operating throughout the country and offering standartized product countrywide. TGMP provides microcredits ranging between 200-600YTL (150-350 US$) with an interest rate of 20 % p.a.a which are distributed on the basis of solidarity groups consisting of five to ten women. The group members are equally accountable for the repayment of loans. The credit receivers use the credits mostly in home-based activities such as raising livestock, petty retail commerce, sewing, and offering other handicraft or small marketing activities in the neighbourhood. The credit programs require borrowers to form groups in which all borrowers are jointly liable for each other's loans.The creation of peer group pressure among the group members encourages each individual in the group to repay her debts regularly enabling the micro credit program to achieve high repayment rates of 98 percent (Rahman 1999). As of October 2012, TGMP operated 94 branches throughout Central and Eastern Turkey,with 60,641 members registered and 183,728 townsands of Turkish lira loaned out by 303 employees. 5 II. The present knowledge base on microcredit is partial and contested. (Kovsted et al., 2000). The state of the art know-how on microfinance is territorial and nontransferable due to cultural uniqueness of every market, and fragmented into many fields of focus, targeting specific topics, while unable to provide a general picture on the characteristics of average client. For young, culturally homogeneous and untapped markets, just as Turkey is, simulation of a credit mannequin presents a way to produce valuable assumptions opportune for the MFIs determined to offer standartized products to mass market clientele with certain sociodemographic traits, reknitting their strategy according to the acquired knowledge during the initial phase of the market development. Credit mannequin, a term introduced for the first time in this study, represents a simulated client model, displaying its most probable characteristics in order to foresee the behavior of the mass clientele in advance. The objective of this synthesis is thus to apprise the average character of the microfinance clientele in Turkey, in the attempt to find socio-demographic patterns of the debtorship, as well as to define a blueprint of the use of loans, access to finance, past experience and nexus with religion. Summarized, the principal goals of the survey are:

1. To assess the socio-economic profile of the average client participating in a successful microfinance program, classified in six key areas. 2. Define remarkable particularities of the Turkish clientele, in relation to three selected assumptions and validate or rejem these. 3. To provide details concerning the socioeconomic traits of microentrepreneurs' households and sectorial activities estimating the potentials and threats influencing development of Turkish microfinance market. Furthermore, the study intends to answer the following questions. What can be said about the average socio-demographic household profile of ideal debtor? Does islamic finance present a competition for classical microfinance? Does religion play an important role for the credit takers? What is the access to finance and what experience have clients with microcredit? Are there any determinants for the turkish microentrepreneurs that are exogenous for the allocation of credit, which could be extrapolated for the future build up of microfinance markets? c) Methodology The primary methodology selected for this study has been a qualitative non-longitudinal approach with percentages of responses being the main data used for the verdict on the client characteristics, based on a standardized questionnaire in which qualitative responses are converted into discrete interval variables, examined with standard correlational tools.The questionnaire consisted out of 30 closed format questions of dichotomous, rating scale and closeended importance types. The selected sample size of the survey was completed by 117 active clients, belonging to the stable core of TGMP portfolio of clients, who answered the questions during weekly ordinary repayment sessions of the TGMP credit groups under the guidance of the credit officer, routinely organised in flats, courtyards or working spaces of the group members.

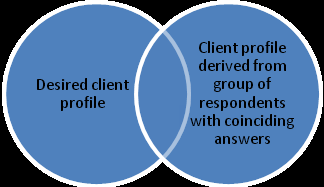

The first part of the study architecture describes the involvement of the debtorship with credit, in six layers of interest: demographic, household, religion, credit experience, credit access and credit use. Presynthesis extended in the second part follows, depicting a model of average turkish microfinance client through those characteristics belonging to the clients whose answers coincide in 50% with the answers from all sample members. In the third part of the study, the clients who according to our view share characteristics desirable by a standard MFI are filtered out and assorted. In the fourth part of the study the two profiles are compared, the average 50% matching profile as well as the desired client profile, in order to obtain credit mannequin profile through profile intersection. The resulting credit mannequin constitutes the most suitable average microcredit client profile in Turkey, ideal target of the MFIs. In the fifth concluding part, we confirm or reject general assumptions and input the credit mannequin into context of current microcredit development in contemporary Turkey, coming to recommendations for expanding/growing microfinance institutions.

2. Research Results

3. a) Classification in six research domains

In the following table we present the questions in the survey classified in six domains. b) Profile of the client group with responses coinciding in more than 50% of the sample The answers to the questions which coincided in over 50% and henceforth present significant reference for the nature of microfinance market, were the following ones: Nr.

4. Question

Answer % of Answers

5. c) Desired client profile

In order to establish the profile of most desired or suitable client out from the sample, the answers to selected questions deemed to deliver positive value to a MFI in terms of its desire to include such respondent in its portfolio, were filtered from the the rest. The resulting profile is derived from the characteristics of these respondents falling into this category in 100% of the answers to selected group of questions. The selection abstains from speculation by choosing only those topics from the survey that undeniably present a simply understandable plus for any MFI, as depicted below.

6. Nr.

Question Desired Answer % of answers The clientele that answered in line with the desired answers was separated from the rest and the responses to all survey questions were processed in percentual charts. The responses from those who fall into the desired client profile are presented below in the respective predetermined six domains. We construct the credit mannequin by allowing the 50% co-incidence profile (3.2.) to intersect with the desired client profile (3.3.) , by filtering the answers matrix field through first and through second filter. The result is the following profile of the ideal microfinance client filtered from the real personalities.

7. Questions

Profile characteristics 6 indicate that competition between islamic credit and village bank microcredit is negligible in Turkey at present, as majority of the clientele stipulated (58.59% and 79.21%) that not many choices are available, nor other credits are accessible from the point of view of price. The resulting answers to question nr. 12 were interpreted as misunderstood, as the clientele considered the term "islamic credit" a synonym for TGMP microcredit. This mere fact however confirms that Shari'ah-compliant credit related literacy is low. In order to test the results on interdependence through statistical methods, we apply the Chi-square test, a measure of the discrepancy between the observed results and hypothetically expected results, with the H0 of no correlation between the group samples.

) ( = 2 2 E E - O ? ?(1)8. O = the observed value E = the expected value

The survey data was input into a table serving the purposes of the analysis, consisting of variables corresponding to number of collected questionnaires, and numbers of economically active people in the household next to suitability mark of the clientele, qualified with marks from -1 to 3 scale, as per answers of every client in the questionnaire, converting qualitative data into quantitative, ordinal data. 8 8 3 points: desired clients as per 3.3; 2 points: ordinary clients as those not falling into categories of desired / less desired / undesired; 1 point: less desired client who answered 1 of the answers to questions in Table 6; 0 points: undesired client with 2 or more indicated answers to the questions in Table 6. According the answers recorded in Table 8, the overwhelming majority of more than 89% of the customers of MFI do not acknowledge having registered any issues in the family / community surrounding, negatively perceiving the act of becoming debtor of a microfinance institution. The assumption C thus cannot be confirmed.

9. Global Journal of

IV.

10. Conclusion

The study provides us with a counterfactual opportunity to combine assumptions on the microfinance market in Turkey with the credit mannequin profile derived out of the intersection of two client profiles based on the field data, and to position the profile of the clientele in the context of contemporary microfinance market in Turkey.

The conclusion can be drawn on basis of the survey that there is no significant competition evidence between Islamic Sharia based credit and classical microcredit. Neither can be confirmed that cultural, religious and community based factors interfere nor influence the debtors in using microcredit, by inspiring distress caused by breach of religious beliefs due to use of interest based microfinance. The number of of the family members co-habiting the same household with the debtors seems not to have an important correlational effect either.

The credit mannequin exercise signposts the sector of retail commerce and small scale production as the most promising markets. It evidences little relevance of age and education for active microcredit clientele, neither regards the current price policy, average loan amounts nor weekly repayments as a matter for reconsideration. On the other hand, the 16 weeks repayment period is considered too short. Past experience with credit can be considered an important positive characteristics to be aimed at when defining new clientele, as well as marital and family status showing as preferent clients married women with 2-3 children, with a strong family background being a robust element of solid debtorship.

This study has shown that the microcredit market in Turkey, however it is influenced by many different factors, is centered around a centre of gravity, which is a family circle. It has not identified major hindrances and indicates high level of flexibility in terms of cultural and communitarian limitations, that will enable its autonomous future development. This page is intentionally left blank

| Socio-Economic Profile of Village Bank Member in Suburban Ankara: Microcredit Mannequin |

| and Assumptions on Microfinance Market of Turkey |

| Credit |

| Mannequin |

| ANSWERS OF 117 SURVEY RESPONDENTS |

| 13 | Is frequency of paying the installments of microcredit for you better than | Yes | 84.00 |

| frequency of other credits? | |||

| 16 | Do social/ family conventions prevent you from becoming a debtor? | No | 89.11 |

| 23 | Does the fact that you are taker of microcredit harm your family/ neighbour | No | 96.00 |

| relationships? | |||

| 24 | Do you recommend your economic active neighbours to take microcredit? | Yes | 95.19 |

| 26 | Are you holder of more than one microcredit at the same time? | No | 58.59 |

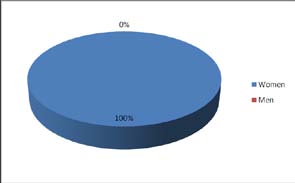

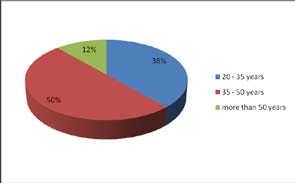

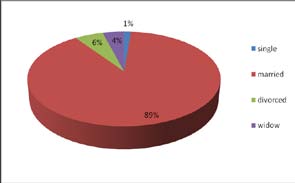

| 1. Sex | 2. Age | 3. Marital Status |

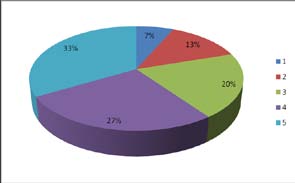

| 4A Children | 4B Number of children |

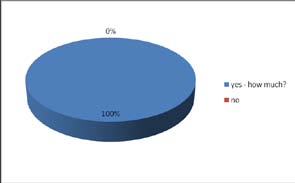

| 27. Do you need | |

| 2013 | |

| ear | |

| Y | |

| ( ) C | |

| e) Confirmation / Rejection of assumptions | 1. Islamic credit presents a competition for microcredit |

| i. Assumptions | of Grameen type. |

| We have established three assumptions that call for | 2. The likelihood of being enrolled in the microcredit |

| corroboration due to the particularity of microfinance | programmes in Turkey is correlated with the number |

| market in Turkey, which differs from the neighbouring | of economically active household members, as the |

| microfinance markets in peculiarity of its state-society | pressure for income originates in the family |

| relationship, religion-state relationship, original culture | environment. |

| and stage of development. Confirmation / rejection of | 3. There is a cultural aversion for microcredit in Turkey, |

| these assumptions will shed more light on the | due to gender and conservative stands of the |

| understanding of the microfinance market in Turkey as a | traditional socio-economic system of a muslim |

| whole and help to position credit mannequin into wider | society. |

| market context. The assumptions follow: |

| 2013 | ||||||

| ear | ||||||

| Y | ||||||

| 69 | ||||||

| Volume XIII Issue VIII Version I | ||||||

| Nr. 16 23 24 26 30 | Question Do social/ family conventions prevent you from becoming a debtor? Does the fact that you are taker of microcredit harm your family/ neighbour relationships? Do you recommend your economic active neighbours to take microcredit? Are you holder of more than one microcredit at the same time? Does your religious leader prevent you from taking microcredit? | Less desired client answer Yes Yes No Yes Yes | C ( ) Management and Business Research | |||

| Value | df | Asymp. Sig. (2-sided) | ||||

| Pearson Chi-square | 9,118681 | 10 | 0,520879 | |||

| No. in | Yes in | ||

| Nr. | Question | % | % |

| 30 | Does your religious leader prevent you from taking microcredit? | 91.00 | 9.00 |

| 16 | Do social/ family conventions prevent you from becoming a debtor? | 89.11 | 10.89 |

| 23 | Does the fact that you are taker of microcredit harm your family/ neighbour relationships? | 96.00 | 4.00 |